Understanding Trial Balance: A Comprehensive Study for Accountants

Trial Balance is a foundational pillar in the world of accounting, essential for both the practice and understanding of financial management. This study offers an in-depth exploration of trial balance for students, aspiring accountants, and those looking to enhance their accounting skills.

From its structure to its significance, from preparation to error identification, we dive into every aspect to offer a complete understanding that serves as a pathway to mastery in the accounting field.

Are you ready to simplify your financial management and streamline your trial balance process?

Are you ready to simplify your financial management and streamline your trial balance process?

Trail Balance

The concept of Trial Balance has a rich history that dates back to the era of early commerce and trade. The systematic comparison began to take shape in the double-entry bookkeeping system popularized in the Renaissance period. The technique has since evolved, incorporating modern computational tools and software to achieve accuracy and efficiency.

In earlier times, trial balances were prepared manually, involving painstaking efforts to ensure that the debit and credit sides were equal. Over time, the methods and practices changed, paving the way for sophisticated accounting software that simplifies the process, reduces human errors, and provides insightful analysis.

How Trial Balance Principles Have Shaped Modern Accounting:

The principles underlying the Trial Balance have had a profound impact on the way modern accounting functions. The need for balancing debits and credits gave rise to the fundamental accounting equation:

Assets = Liabilities + Equity

This concept underpins financial reporting and analysis and ensures that a company's books are transparent and balanced.

Trial Balance has fostered standardization and uniformity in accounting practices, laying the groundwork for international accounting standards. It continues to be a crucial part of financial management, serving as a checkpoint for accountants to verify that all transactions have been accurately recorded.

Different Types of Trial Balances

Unadjusted, Adjusted, and Post-Closing Trial Balances:

Trial balances are not all the same; they come in three primary variations that correspond to different stages in the accounting cycle. These include:

Unadjusted Trial Balance: This is the initial trial balance prepared at the end of an accounting period but before any adjustments have been made for accrued expenses, revenues, etc. It's a crucial step in identifying discrepancies and ensuring that debits equal credits before proceeding with any modifications.

Adjusted Trial Balance: After making necessary adjustments for accruals, deferrals, and other accounting necessities, an adjusted trial balance is prepared. This reflects the true financial standing of the company, including all transactions and necessary corrections. It forms the basis for the preparation of financial statements such as the income statement and balance sheet.

Get 30% Off Wafeq yearly packages

Enter your email to receive your exclusive discount code. New users only!

Post-Closing Trial Balance: This version comes after the closing entries have been made, reflecting only the balance of the permanent or real accounts. Temporary accounts like revenues, expenses, and dividends are closed, and the balance is transferred to the capital or retained earnings accounts. It serves as a starting point for the next accounting cycle, ensuring the accounts are ready for the new period.

How Each Type is Used Within the Accounting Cycle:

- Unadjusted Trial Balance: Used to check initial accuracy before adjustments.

- Adjusted Trial Balance: Forms the basis for financial statements, reflecting the true financial condition.

- Post-Closing Trial Balance: Acts as a foundation for the next accounting period, closing temporary accounts.

Read More: 5 Reasons Why You Need An Invoice Maker Online For Your Business.

Integration of Trial Balance with Other Financial Statements

The trial balance serves as a pivotal point in the accounting process, linking various financial statements together. Here's how it integrates with them:

How the Trial Balance Interacts with Balance Sheets, Income Statements, etc.:

Balance Sheet: The adjusted trial balance is used to compile the balance sheet, as it reflects the company's financial position at a specific point in time, including assets, liabilities, and equity.

Income Statement: The adjusted trial balance also feeds into the income statement, summarizing revenues and expenses to calculate net income for a particular period.

Cash Flow Statement: Information from the adjusted trial balance can be used to determine cash flows from operating, investing, and financing activities.

The Flow of Information from the Trial Balance to Other Financial Reports:

Sequential Process: The unadjusted trial balance serves as a preliminary check, leading to adjustments, which in turn form the adjusted trial balance. This then becomes the basis for generating various financial statements.

Data Consistency: The trial balance ensures consistency across all financial reports, maintaining alignment between different accounting records.

Error Detection and Correction: The trial balance's inherent structure allows for early detection and correction of discrepancies, ensuring the accuracy of subsequent financial statements.

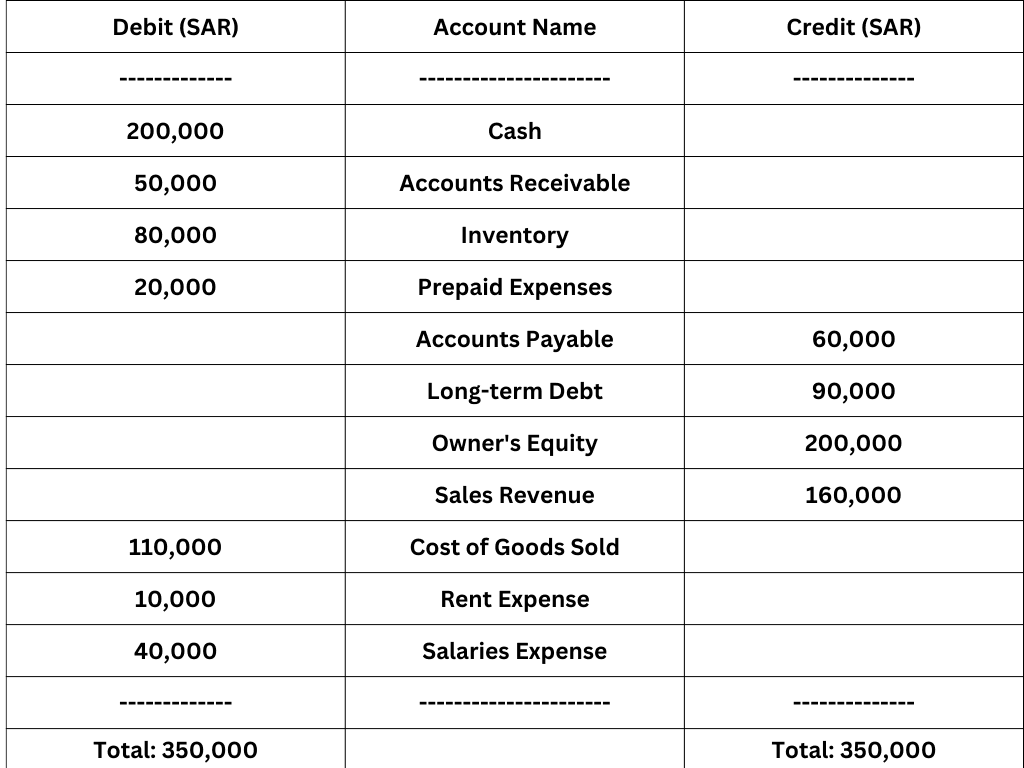

Example of Trail Balance:

Trial Balance in Different Industries:

The implementation and use of trial balance can vary widely across industries. Each sector has its unique challenges and requirements that shape how the trial balance is utilized. Let's explore these considerations:

Specific Considerations for Trial Balance in Different Sectors:

Retail: In retail, trial balance must take into account seasonal fluctuations and promotions. Accurate reporting helps in inventory management and pricing strategies.

Manufacturing: Manufacturing businesses often have complex supply chain considerations. Trial balance here requires keen attention to raw materials, production costs, and overheads.

Services: The service industry deals with intangible goods, so the trial balance must include considerations for things like contracts, labor costs, and deferred revenue.

Read also: The Importance of Trial Balance for Business Owners.

Advanced Techniques and Tips for Managing Trial Balance

The management of trial balance requires precision, efficiency, and adaptability. Using advanced techniques and software features can make this task more manageable and accurate. Here's an in-depth look:

Utilizing Advanced Software Features:

- Automation & Integration: Software like Wafeq provides automation of trial balance entries, and integration with other financial modules, simplifying the process.

- Real-time Analysis: Tools offering real-time analytics help in instant error detection and corrective action.

- Customizable Reporting: Advanced reporting tools enable customization to fit industry standards, especially in Saudi Arabia's diverse business landscape.

Future of Trial Balance in the Age of Automation and AI

The rapid development automation and AI is revolutionizing the way trial balance is managed. Here's how:

- Transforming Trial Balance Management:

Automated Entries & Analysis: Tools are now available that can automatically input data, analyze, and detect errors in the trial balance, reducing human error.

AI-Powered Insights: Intelligent algorithms can predict future trends, providing insights for decision-making, especially pertinent for businesses in Saudi Arabia's dynamic market.

- Potential Future Trends and Innovations

Integration with Other AI Systems: Future tools may allow seamless integration with other AI-driven business processes.

Personalized Solutions: Tailored approaches to trial balance may emerge, catering to specific industry needs.

Global Perspectives on Trial Balance

Trial balance principles and practices vary significantly across different countries and regions. An understanding of these differences is essential:

Differing Principles and Practices

Accounting Standards: Different countries have distinct accounting rules, affecting the way trial balance is prepared and analyzed.

Regulatory Compliance: Regulations can differ widely, influencing the preparation and use of the trial balance.

Frequently Asked Questions (FAQ) about Trial Balance

1. What is a Trial Balance?

A Trial Balance is a report that lists all the general ledger accounts and their balances at a specific point in time. It serves as a preliminary check to ensure that total debits equal total credits, verifying the accuracy of the bookkeeping entries.

2. Why is a Trial Balance Important?

A Trial Balance is crucial because it helps detect errors in the accounting records, ensures the accuracy of financial statements, and provides a snapshot of a company’s financial position. It is an essential step in the accounting cycle before preparing formal financial statements.

3. How is a Trial Balance Prepared?

A Trial Balance is prepared by listing all the ledger accounts and their balances, ensuring that total debits equal total credits. Here's a step-by-step process:

- Extract balances from the general ledger.

- List accounts with their debit or credit balances.

- Sum up debit and credit columns.

- Check for equality between total debits and credits.

4. What are Common Errors Detected by a Trial Balance?

Common errors detected by a Trial Balance include:

Transposition Errors: Numbers are recorded incorrectly due to reversing digits.

Omission Errors: Missing transactions or entries.

Duplication Errors: Recording the same transaction more than once.

Calculation Errors: Incorrect arithmetic operations leading to imbalances.

5. What Happens if the Trial Balance Doesn’t Balance?

If the Trial Balance doesn't balance, it indicates potential errors in the accounting records. Accountants must review the entries, check for any omissions or duplications, and correct any discrepancies to achieve a balanced state.

6. What are the Differences Between Unadjusted, Adjusted, and Post-Closing Trial Balances?

- Unadjusted Trial Balance: Prepared before any adjustments, reflecting initial balances.

- Adjusted Trial Balance: Includes necessary adjustments for accruals and deferrals, forming the basis for financial statements.

- Post-Closing Trial Balance: Reflects only permanent accounts after closing temporary accounts, serving as a starting point for the next accounting period.

7. How Does a Trial Balance Integrate with Other Financial Statements?

A Trial Balance integrates with other financial statements by providing the foundational data needed to compile the Balance Sheet, Income Statement, and Cash Flow Statement. The adjusted Trial Balance ensures consistency and accuracy across all reports.

8. How is Technology Transforming Trial Balance Preparation?

Modern accounting software automates Trial Balance preparation, reducing manual errors and increasing efficiency. AI-powered tools provide real-time analysis, error detection, and customizable reporting, enhancing the accuracy of financial management.

9. What are the Best Practices for Managing Trial Balance in Different Industries?

Different industries have unique challenges that affect Trial Balance management:

- Retail: Consider seasonal fluctuations and inventory management.

- Manufacturing: Focus on raw materials, production costs, and overheads.

- Services: Account for contracts, labor costs, and deferred revenue.

10. How Do International Standards Affect Trial Balance?

International standards like IFRS promote consistency and comparability in Trial Balance preparation. They facilitate cross-border transactions and collaborations, aligning accounting practices with global norms.

11. Can a Trial Balance Identify All Types of Errors?

While a Trial Balance can detect many errors, it cannot identify all types. Errors such as compensating errors, errors of principle, and complete omission errors may not be revealed through a Trial Balance alone. Further analysis and internal controls are necessary for comprehensive error detection.

12. How Often Should a Trial Balance be Prepared?

A Trial Balance should be prepared regularly, typically at the end of each accounting period (monthly, quarterly, or annually), to ensure accurate and up-to-date financial records. Regular preparation helps maintain the integrity of the financial statements.

International Standards and Their Impact

IFRS & Other Global Standards: Adoption of International Financial Reporting Standards (IFRS) or other global guidelines affects the consistency and comparability of trial balance.

Cross-Border Collaboration: International standards facilitate cross-border transactions and communication between businesses, making it easier to operate globally.

Discover Wafeq - the ultimate financial solution designed to meet the unique needs of your business.

Discover Wafeq - the ultimate financial solution designed to meet the unique needs of your business.

.png%3Falt%3Dmedia&w=3840&q=75)