Understanding Cost Accounting: A Comprehensive Guide to Cost Management and Decision Making

Introduction to Cost Accounting

Definition and Purpose: Cost accounting refers to the process of recording, classifying, analyzing, and summarizing costs associated with the production or service provision. Its primary purpose is to provide detailed information for decision-making, cost control, and performance evaluation.

Importance in Business Management: In the business landscape, cost accounting plays a crucial role in budgeting, pricing strategies, and profitability analysis. It assists management in making informed decisions that align with organizational goals.

Historical Background: Cost accounting has evolved over time, adapting to changes in industrial practices and economic conditions. Its origins can be traced back to the industrial revolution when the need for accurate cost information became vital.

Experience the future of cost accounting today with Wafeq's advanced tools that offer precision, compliance, and real-time insights tailored to your market.

Experience the future of cost accounting today with Wafeq's advanced tools that offer precision, compliance, and real-time insights tailored to your market.

Types of Costs

Fixed Costs: These are expenses that remain constant regardless of the level of production or service provision. Examples include rent, salaries, and insurance.

Variable Costs: Unlike fixed costs, variable costs change with the level of production. These include costs of raw materials, packaging, and transportation.

Direct Costs: Direct costs are associated specifically with the production of a product or delivery of a service. They include labor costs, material costs, and manufacturing overhead.

Get 30% Off Wafeq yearly packages

Enter your email to receive your exclusive discount code. New users only!

Indirect Costs: Indirect costs are general expenses that support the overall business operations but cannot be directly linked to a specific product or service. These include administrative expenses, utilities, and advertising.

Opportunity Costs: This refers to the potential benefits that an individual or business misses out on when choosing one alternative over another. It's the value of the best alternative forgone, and it plays a vital role in decision-making.

Read more: Inventory Management: A Comprehensive Understanding of Periodic and Perpetual Inventory.

Methods of Cost Accounting

In the intricate realm of business finance, cost accounting is a pivotal component. Understanding the cost structure is vital for making informed decisions that align with the company’s strategic goals. Here's an exploration of various cost accounting methods:

Total Cost Method:

This traditional approach includes all costs, aligning with general accounting principles. Its main drawback is the lack of specific cost identification.

Partial Cost Method:

Dividing the costs into different categories, this method discerns between fixed and variable costs, direct and indirect costs, and further classifies into:

- a. Variable Costs: Separates fixed and variable costs, mainly focusing on variable ones.

- b. Direct Costs: Differentiates between direct and indirect costs, charging the product with direct costs only.

- c. Exploited Costs: Combines variable costs with a portion of fixed costs, known for its simplicity.

- d. Standard Costs: Based on planned budgets, it allows for the comparison between predefined and actual costs to find variances.

Other Costing Methods:

- Actual Cost/Actual Output Method: Examines all the recorded costs in a project.

- Average Cost Method: Works on assigning inventory costs by calculating the moving average.

- First-In-First-Out (FIFO) Method: A widely recognized formula that follows the first item's entry and exit pattern.

- Cost-to-Cost Formula: Incorporates all costs in a process, considering both direct and indirect expenses.

Read more: Cost Competitiveness In Business: How To Win The Race.

Cost Accounting in Different Industries

Cost accounting methodologies are not confined to a specific sector; they permeate through various industries, each with unique requirements and challenges:

Manufacturing:

Cost accounting in manufacturing deals with allocating direct and indirect costs to produce goods. Methods like Activity-Based Costing (ABC) are commonly used to identify the cost drivers in production, enabling more accurate pricing and profitability analysis.

Services:

In the service industry, cost accounting emphasizes labor and overhead costs. It helps in understanding the cost structure of delivering specific services and creating pricing strategies that reflect value and competitiveness.

Retail:

Retail businesses often employ cost accounting to manage inventory and identify the optimal markup. Techniques such as the First-In-First-Out (FIFO) method help in tracking inventory costs, thus enhancing decision-making in stock control and pricing.

Healthcare:

Cost accounting in healthcare involves analyzing the expenses related to patient care, including medical supplies, staff wages, and administrative costs. It provides insights into cost efficiency and aids in determining areas for improvement and cost containment.

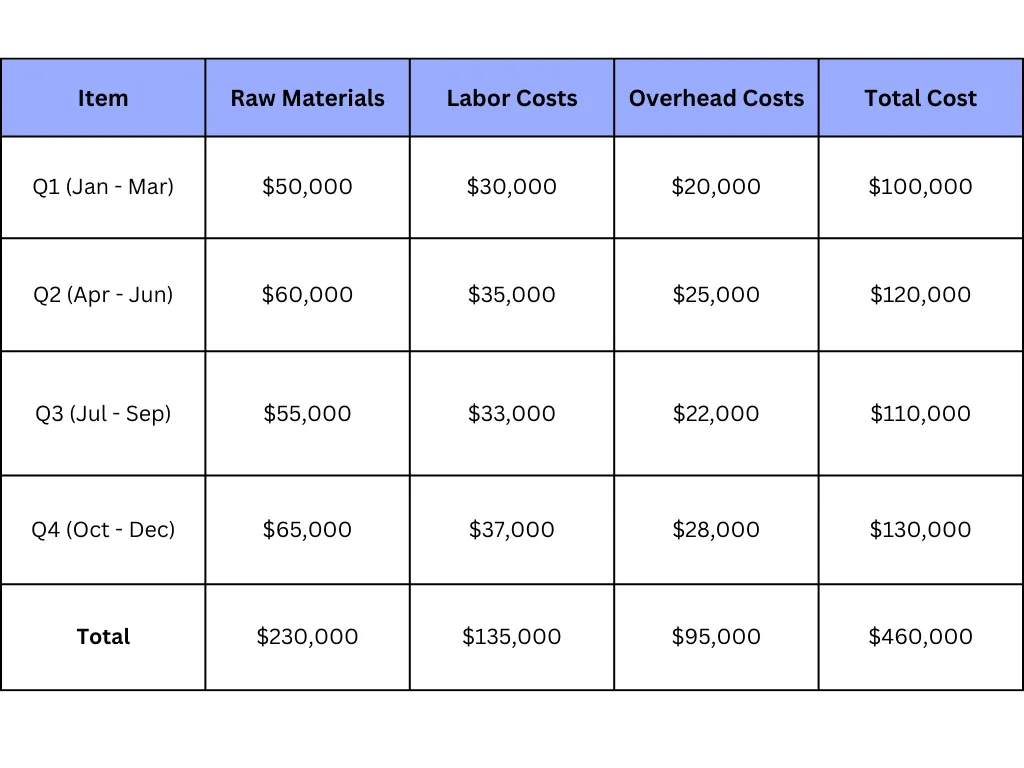

Example of Cost Accounting:

Challenges in Cost Accounting

Cost accounting, despite its fundamental role in financial management, faces several challenges that can impact the accuracy and efficiency of the process:

Accuracy in Estimation:

Estimating costs accurately is critical for budgeting, pricing, and overall financial planning. A minor error can lead to significant misjudgments in financial decisions. The difficulty in predicting future costs and the variability of certain expenses make this a daunting task.

Complexity of Allocation:

Allocating costs between different departments or products can become highly complex, especially when dealing with indirect costs. It requires a deep understanding and analysis of cost drivers, leading to potential conflicts and misconceptions.

Changes in Technology and Practices:

The rapidly evolving technological landscape and changes in industrial practices necessitate continuous adaptation in cost accounting methods. This ever-changing environment can create uncertainty and necessitate constant updates to methodologies and systems.

Compliance with Regulations:

Different jurisdictions have different regulations and standards for cost accounting. Compliance with these regulations is paramount but can be complicated, time-consuming, and costly, especially for businesses operating in multiple regions like in Saudi Arabia.

Role of Cost Accounting in Decision Making

Cost accounting plays a vital role in strategic decision-making within businesses. Its influence permeates various aspects of financial planning and control, shaping the future of the company. Here's an insight into how cost accounting affects different areas:

Pricing Strategies:

Informed Decisions: Cost accounting allows businesses to determine accurate product costs, aiding in the formulation of competitive pricing strategies.

Saudi Market Example: Saudi businesses, including those in the manufacturing and retail sectors, utilize cost accounting to set prices that align with market demands and their overall business goals.

Budgeting and Forecasting:

Strategic Planning: Budgeting and forecasting tools in cost accounting offer a roadmap for financial planning, enabling companies to allocate resources efficiently.

Real-world Application: In Saudi Arabia, many organizations use cost accounting for better planning of their yearly budgets, capital expenditures, and revenue forecasts.

Cost Control and Reduction:

Operational Efficiency: Cost accounting promotes efficiency by identifying areas for potential savings and implementing cost control measures.

Performance Evaluation:

Employee Assessment: Cost accounting helps in evaluating the performance of various departments and employees, ensuring alignment with organizational objectives.

Read more: Cost Centers: An In-Depth Guide to Understanding and Managing Costs

Conclusion

Cost accounting, a multifaceted and critical component in various business operations, drives pricing strategies, budgeting, forecasting, cost control, and performance evaluation. In a complex and evolving business landscape, including in the Saudi market, it enables companies to make informed decisions in alignment with market needs. The field is expected to evolve further with technological advancements and a focus on data-driven insights. Practitioners must embrace the latest technologies, strive for accuracy, stay compliant with changes in regulations, and continuously monitor performance. In Saudi Arabia, the integration of artificial intelligence and other modern tools will likely shape the future of cost accounting, allowing for more precise and real-time analysis.

Are you ready to transform your cost accounting practice with modern technology? Wafeq's cutting-edge solutions align with global best practices and are designed to streamline your accounting needs.

Are you ready to transform your cost accounting practice with modern technology? Wafeq's cutting-edge solutions align with global best practices and are designed to streamline your accounting needs.

.png?alt=media)