Aging Reports Explained: Step-by-Step Guide to Managing Receivables Effectively

At month-end, financial reports may reflect solid sales and issued invoices, yet cash inflows often tell a different story. Outstanding receivables, delayed customer payments, and unclear collection priorities can quickly turn reported revenue into a cash flow concern. Without visibility into how long receivables have been outstanding, financial decisions lose accuracy.

This is where the Aging Report (Accounts Receivable Aging Report) becomes essential, offering a structured view of receivables by aging periods to support effective credit management and cash collection.

Key Takeaways:

- Understand what an Aging Report is and why it matters.

- Learn how businesses use aging data to improve cash flow visibility.

- Identify early warning signs of collection risk and bad debts.

- Discover practical insights accountants search for when analyzing aging reports.

What Is an Aging Report (Accounts Receivable Aging Report)?

An Aging Report, also known as an Accounts Receivable Aging Report, is a financial report that shows how long customer invoices have remained unpaid. Instead of listing receivables as a total number, the report classifies outstanding balances into time-based buckets, helping finance teams understand payment behavior and collection risk.

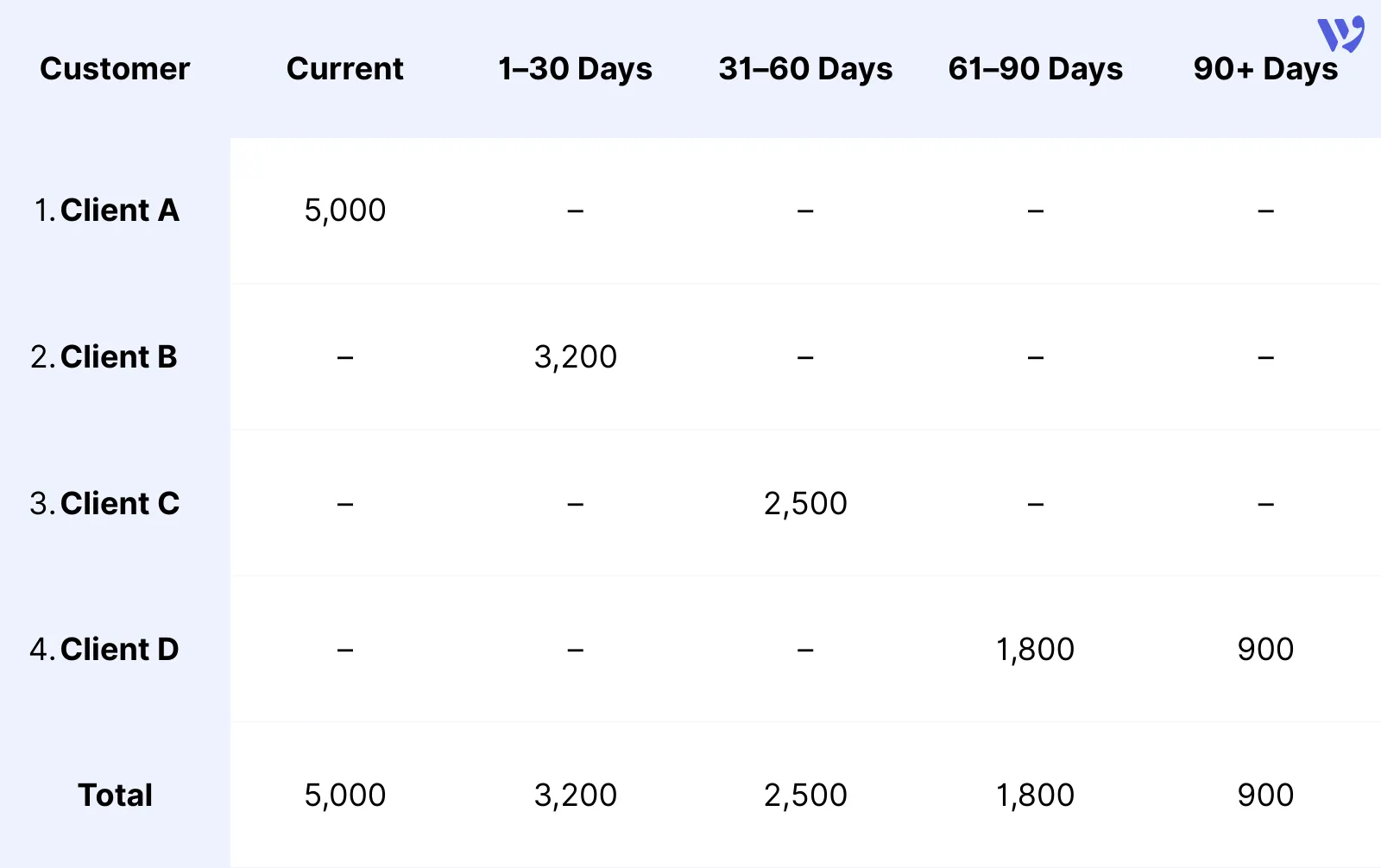

Most aging reports are divided into standard periods, such as:

- Current (not yet due)

- 1–30 days overdue

- 31–60 days overdue

- 61–90 days overdue

- Over 90 days overdue

By breaking receivables into these intervals, businesses can clearly see which amounts are still healthy and which require immediate follow-up.

Why the Aging Report Is More Than Just a List of Invoices

Get 30% Off Wafeq yearly packages

Enter your email to receive your exclusive discount code. New users only!

What makes the aging report powerful is not the data itself, but how it supports decisions. It turns receivable data into actionable insight, not just accounting records, and helps businesses:

- Prioritize collection efforts.

- Assess customer creditworthiness.

- Estimate potential bad debts.

- Improve cash flow forecasting.

Key Components of an Aging Report (And How to Read It)

An Aging Report follows a simple structure, but reading it correctly is what makes the difference. Each column tells a story about customer payment behavior and potential cash flow risk.

Main Components of an Aging Report

- Customer Name: Identifies who owes the balance.

- Invoice Number: Helps trace the original transaction.

- Invoice Date: Indicates when the invoice was issued.

- Due Date: Shows when payment was expected.

- Outstanding Balance: The unpaid amount.

- Aging Buckets: Time-based categories that show how overdue the balance is.

To make this clearer, here’s a simplified example.

How to Interpret the Report

- Higher balances in “Current” or “1–30 Days” usually indicate healthy collections.

- Amounts in “61–90 Days” or “90+ Days” signal higher risk and require immediate action.

- A growing 90+ Days balance may indicate weak credit policies or collection delays.

Finance teams often review this report weekly or monthly to adjust credit terms and collection priorities.

Finance teams often review this report weekly or monthly to adjust credit terms and collection priorities.

Why Do Businesses Rely on the Aging Report?

Businesses do not use the Aging Report just for record-keeping. It is a practical management tool that supports daily financial decisions, especially for companies offering credit sales.

Here are the main reasons finance teams consistently rely on it:

1. Improving Cash Flow Management The report highlights overdue receivables before they become a serious cash flow issue. By focusing on aging balances, businesses can accelerate collections and reduce reliance on external financing.

2. Prioritizing Collection Efforts Not all overdue invoices require the same response. The Aging Report helps teams:

- Follow up gently on recent delays.

- Escalate action on long-overdue balances.

- Allocate collection resources efficiently.

3. Assessing Customer Credit Risk Customers who consistently appear in older aging buckets may indicate higher credit risk. This insight supports better decisions around:

- Credit limits.

- Payment terms.

- Future sales on credit.

4. Estimating Bad Debts Aging data is commonly used to estimate allowance for doubtful accounts, especially for balances exceeding 90 days. This supports more accurate financial reporting and compliance with accounting standards.

How to Analyze an Aging Report Effectively (Step-by-Step)

Reviewing an Aging Report without a clear approach can lead to missed risks or delayed action. Follow these steps to turn the report into a practical decision-making tool.

- Review the Total Outstanding Balance Start by looking at the total receivable amount. A sudden increase compared to previous periods may indicate slower collections or changes in customer payment behavior.

- Focus on Older Aging Buckets Pay close attention to balances in the 61–90 days and 90+ days categories. These amounts carry a higher risk of non-collection and should be prioritized.

- Identify Repeated Late Payers Look for customers who consistently appear in overdue categories. This pattern often signals structural payment issues rather than one-time delays.

- Compare Aging Trends Over Time Analyze how balances move between aging buckets month over month. Healthy collections should show amounts shifting back to “Current,” not accumulating in older buckets.

- Align Actions with Aging Results Use the analysis to:

- Adjust credit terms.

- Trigger follow-up or legal action.

- Update bad debt provisions.

- Support cash flow forecasts.

Common Mistakes When Using an Aging Report

Even though the Aging Report is a powerful tool, its value can be reduced if it is used incorrectly. Here are some common mistakes businesses make when analyzing aging data.

- Focusing Only on Total Receivables Looking at the total outstanding balance without analyzing aging buckets can hide serious collection risks. A stable total may still include an increasing number of long-overdue invoices.

- Ignoring Long-Overdue Balances Allowing invoices in the 90+ days category to remain unaddressed increases the likelihood of non-collection. These balances should trigger immediate review and action.

- Not Updating the Report Regularly Using outdated aging data leads to delayed decisions. The report should be reviewed frequently, weekly or monthly, depending on business size and transaction volume.

- Treating All Customers the Same Applying the same follow-up approach to all overdue customers ignores differences in payment history and credit risk. Aging data should support tailored collection strategies.

- Disconnecting Aging Analysis from Accounting Entries Failing to link aging results with bad-debt provisions and write-offs can distort financial statements and reduce reporting accuracy.

How Accounting Software Automates the Aging Report

Modern accounting software has transformed the Aging Report from a static spreadsheet into a real-time financial tool. Instead of manual calculations and updates, systems now generate aging data automatically based on invoices, due dates, and customer payments.

Here’s how automation adds real value:

1. Real-Time Aging Calculations Accounting software automatically classifies receivables into aging buckets based on invoice dates and payment terms. This ensures the report is always up to date without manual intervention.

2. Reduced Errors and Manual Effort Manual aging reports are prone to formula errors and outdated data. Automation minimizes human error and saves time, especially for businesses with high transaction volumes.

3. Drill-Down Visibility Most systems allow users to click on aging balances and view:

- Individual invoices.

- Payment history.

- Credit notes and adjustments.

4. Better Credit Control Automated aging reports support credit decisions by:

- Flagging overdue customers.

- Supporting credit limit enforcement.

- Linking aging data to customer profiles.

5. Integration with Financial Reporting Aging data feeds directly into:

- Cash flow forecasts.

- Allowance for doubtful accounts.

- Management and audit reports.

Read Also: Accounts Receivable Accountant: Responsibilities and Impact on Cash Flow

An Aging Report is more than just numbers—it’s a vital tool for managing accounts receivable, improving cash flow, and reducing financial risk. By analyzing overdue invoices, tracking customer payment behavior, and using automation tools like Wafeq, businesses can make smarter credit decisions and maintain healthy financial operations.

FAQ About Aging Reports

How often should I generate an Aging Report?

Ideally, weekly for fast-moving businesses, or at least monthly for standard operations. Frequent updates help detect overdue invoices early.

Can I use an Aging Report for cash flow forecasting?

Yes. Aging data provides insight into expected inflows and highlights potential shortfalls, making it easier to plan for working capital needs.

What is the difference between “Current” and “1–30 Days” categories?

“Current” refers to invoices not yet due, while “1–30 Days” captures invoices overdue by up to 30 days. Both are crucial for tracking payment behavior.

How do I handle long-overdue invoices?

Implement a structured collection strategy that may include reminders, calls, and, in extreme cases, legal action. Aging Reports help prioritize these steps.

Can software help with audit compliance?

Absolutely. Automated aging reports provide clear evidence of receivables and collection actions, supporting audit requirements and regulatory compliance.

With Wafeq Accounting Software, you can gain full control over your accounts receivable, making collections smoother and cash flow more predictable.

With Wafeq Accounting Software, you can gain full control over your accounts receivable, making collections smoother and cash flow more predictable.

.png?alt=media)