Understanding Accounting Journals: Key Concepts and How to Record

Every business transaction leaves a trace, but those traces can vanish without a journal. Imagine discovering the source of a financial discrepancy months later, only to find no written record of what happened. The journal is the first and most essential step in accounting. a chronological record that preserves the company's financial memory. It brings clarity, supports transparency, and ensures every decision is traceable. Whether for internal analysis or external audits, the strength of a company’s financial reporting begins with the precision of its journal.

What Is a Journal in Accounting?

A journal in accounting is a chronological record of all financial transactions within a business. It’s the initial place where transactions are documented before being posted to the ledger. Each journal entry includes the transaction date, accounts involved, amounts debited and credited, and a brief description. Recording in the journal follows the double-entry system, which ensures every transaction affects at least two accounts, one debit and one credit, with equal values.

Importance of the Journal in the Accounting Cycle

The journal plays a foundational role in the accounting process for several reasons:

- Accurate Financial Reporting: Errors are reduced when transactions are properly recorded at the source.

- Audit Trail: Each entry offers transparency, enabling internal and external audits.

- Decision Making: Management relies on accurate journal entries to assess performance and allocate resources.

- Regulatory Compliance: Maintaining organized records is a legal requirement in many jurisdictions, including Saudi Arabia.

Components of a Journal Entry

Get 30% Off Wafeq yearly packages

Enter your email to receive your exclusive discount code. New users only!

A standard journal entry includes:

- Date of the transaction.

- Accounts affected.

- Amount debited.

- Amount credited.

- Narration or explanation

- Reference number (optional)

Types of Journal Entries

There are several types of journal entries, each serving a specific purpose:

- Simple Entry: Involves only one debit and one credit account.

- Compound Entry: Involves more than one debit or credit account.

- Adjusting Entry: Made at the end of a period for accruals or deferrals.

- Opening Entry: Records the opening balances at the beginning of the accounting period.

- Closing Entry: Transfers temporary account balances to permanent accounts at period-end.

- Correcting Entry: Fixes an error in a previously recorded entry.

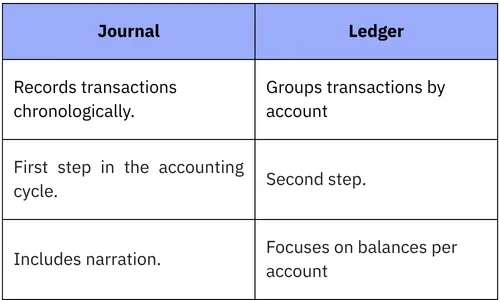

Journal vs Ledger: What’s the Difference?

Step-by-Step: How to Record a Journal Entry

Before recording any journal entry, It’s essential to follow a consistent method to ensure accuracy and compliance. The process may seem simple, but each step plays a critical role in maintaining the integrity of your financial records.

- Identify the nature of the transaction.

- Determine which accounts are affected.

- Decide which account to debit and which to credit.

- Enter the transaction with amounts and narration.

- Reference the document (invoice, receipt, etc.)

- Review and post to the ledger.

Real-Life Examples of Journal Entries

Journal entries are not theoretical; they reflect the daily reality of business transactions. Below are some common scenarios to illustrate how journal entries are used in practice. Each example shows the affected accounts, whether they are debited or credited, and provides a brief.

Example 1: Purchase of office supplies

Example 1: Purchase of office supplies

Debit: Office Supplies (Expense)

Credit: Cash or Accounts Payable

Example 2: Sale to a customer on credit

Example 2: Sale to a customer on credit

Debit: Accounts Receivable

Credit: Sales Revenue

Example 3: Accrued salary at month-end

Example 3: Accrued salary at month-end

Debit: Salaries Expense

Credit: Salaries Payable

Example 4: Depreciation of Equipment

Example 4: Depreciation of Equipment

Debit: Depreciation Expense

Credit: Accumulated Depreciation

Common Mistakes in Journal Entries and How to Avoid Them

Even experienced accountants can make mistakes when recording journal entries. These errors, if not identified early, can lead to misstatements in financial reports, audit issues, and even legal consequences. Understanding the common pitfalls and how to avoid them is crucial for maintaining accurate records.

- Reversing Debit and Credit Accounts One of the most frequent errors is recording the debit and credit on the wrong accounts. This can distort financial statements and lead to misinterpretation.

- Omitting Transactions Failure to record a transaction entirely is a serious issue that can result in incomplete financial data.

- Using Incorrect Account Titles Assigning a transaction to the wrong account title may not affect the balance, but can misclassify the nature of expenses or income.

- Missing Narrations or Explanations Not providing a clear explanation for a journal entry makes it difficult to understand or justify later.

- Not Following Double-Entry Rules Each journal entry must balance debits and credits. Skipping this rule results in an unbalanced ledger and flawed reports.

Digital Journals and Accounting Software

The traditional paper-based journal is rapidly being replaced by digital journals powered by modern accounting software. Digital journals offer significant advantages, including speed, accuracy, and ease of access. They allow businesses to record transactions instantly, with automated calculations that eliminate manual errors. Using accounting softwareJournal entries can be generated automatically based on bank feeds, invoices, and other integrated data sources. This automation reduces repetitive work and improves efficiency, enabling accountants to focus on analysis rather than data entry.

Moreover, digital journals provide real-time updates and comprehensive audit trails. This transparency supports better financial control, easier compliance with regulatory requirements, and simplifies audits. Cloud-based solutions also offer remote access, ensuring that financial data is secure yet available anywhere, anytime.

How to record journals in Wafeq

Watch the video for detailed steps:

Read Also about: Accounting Journals, Ledgers, And Double Entry.

Maintaining an accurate and well-organized journal is essential for any business’s financial health. It ensures compliance with accounting standards and regulations and also provides a reliable foundation for decision-making and financial analysis. Understanding how to record properly, review, and correct journal entries is a fundamental skill for finance professionals.

FAQs about the Journal of Accounting

Can a journal entry be reversed?

Yes, a journal entry can be reversed if it was recorded incorrectly or needs to be canceled. Reversing entries are common at the beginning of an accounting period to correct accrued expenses or revenues. However, reversing should be done carefully to avoid creating new errors.

How long should journal records be kept?

The retention period for journal records varies by country but generally ranges from 5 to 10 years. In Saudi Arabia, companies must keep accounting records, including journals, for at least 10 years to comply with legal and tax regulations.

What is the difference between adjusting and correcting entries?

Adjusting entries update accounts at the end of an accounting period to reflect earned revenues or incurred expenses that haven't been recorded yet. Correcting entries fixes errors made in previous journal entries, such as misclassifications or incorrect amounts.

Is it mandatory to include narration in each journal entry?

While not always mandatory, including a clear narration or explanation for each journal entry is highly recommended, as it helps anyone reviewing the records to understand the nature and purpose of the transaction, facilitating audits and future references.

What happens if there is an error in a journal entry?

Errors in journal entries can lead to inaccurate financial statements, which may mislead management, investors, or regulators. They can also cause audit issues and potentially legal penalties. Therefore, it is important to identify and correct errors promptly.

Ready to streamline your journal entries and improve financial accuracy? Discover how Wafeq can automate and simplify your accounting workflow today.

Ready to streamline your journal entries and improve financial accuracy? Discover how Wafeq can automate and simplify your accounting workflow today.

.png?alt=media)