How to Value a Business Using Discounted Cash Flows (DCF): Step-by-Step Guide

_ دليل مفصّل للتقييم المالي.png?alt=media)

In corporate finance, understanding the true worth of an investment often extends beyond reported profits or growth projections. A company may appear profitable on paper, yet its future cash flows might not justify its current valuation. This distinction between accounting performance and economic value forms the foundation of the Discounted Cash Flow (DCF) approach, a critical method financial professionals use to determine the present value of expected future cash inflows. By quantifying how the value of money changes over time, DCF provides a clearer and more accurate assessment of an asset’s or a company’s financial worth, enabling sound investment, budgeting, and valuation decisions.

What is Discounted Cash Flow (DCF)?

The Discounted Cash Flow (DCF) method is a fundamental valuation approach used to estimate the present value of future cash flows generated by a business, project, or investment. It rests on one central principle in finance, the time value of money, which asserts that a unit of currency today is worth more than the same unit in the future due to its earning potential.

In practice, DCF involves projecting future cash inflows and outflows, then discounting them back to their present value using a rate that reflects the cost of capital or the risk profile of the investment. The result provides an actual measure of what those future earnings are worth today.

Financial professionals rely on DCF to make strategic decisions such as valuing companies, assessing project feasibility, determining acquisition prices, or evaluating investment returns. DCF delivers a more accurate picture of an asset’s intrinsic value by focusing on actual cash generation rather than accounting profits. As DCF answers a critical question for every investor or finance manager: “How much are future cash flows worth today?”

What are The Core Components of DCF?

Any Discounted Cash Flow (DCF) analysis's effectiveness depends on the accuracy of its core components. Each element has a role in determining an investment's present value and reflecting its financial reality.

- Cash Flows Cash flows represent the expected inflows and outflows of money the business or project generates over a specific period. They typically include operating cash flows, capital expenditures, and working capital adjustments. Estimating these flows requires a careful analysis of revenue projections, costs, and future business conditions. The more precise the cash flow forecast, the more reliable the DCF outcome.

- Discount Rate The discount rate reflects the risk and cost of capital associated with the investment. It converts future cash flows into their present value by accounting for the time value of money and the risk premium. Commonly used discount rates include the Weighted Average Cost of Capital (WACC) for businesses and the required rate of return for specific projects. Selecting an appropriate discount rate is one of the most critical steps in DCF valuation.

- Time Horizon The time horizon, or projection period, defines the years for which future cash flows are estimated. Typically, this period ranges from five to ten years, depending on the business model and industry predictability. Longer horizons require greater caution due to the uncertainty of long-term forecasts.

- Terminal Value Since it’s not feasible to forecast cash flows indefinitely, the terminal value captures the value of cash flows beyond the projection period. It usually accounts for a significant portion of the total valuation and can be calculated using the perpetuity growth model or the exit multiple method. Including a well-calculated terminal value ensures the DCF model reflects the ongoing value of the business after the forecast period.

How to Calculate Discounted Cash Flow — Step-by-Step

Get 30% Off Wafeq yearly packages

Enter your email to receive your exclusive discount code. New users only!

Calculating Discounted Cash Flow (DCF) involves a structured approach that measures the present value of expected future cash inflows. The process combines financial forecasting, risk assessment, and mathematical precision to derive a fair valuation.

- Step 1: Estimate Future Cash Flows Start by forecasting the annual free cash flows the investment or project is expected to generate. These are typically calculated as: Free Cash Flow (FCF) = Operating Cash Flow − Capital Expenditures Cash flow projections usually span five to ten years, depending on the business and industry predictability.

- Step 2: Determine the Discount Rate The discount rate reflects the required rate of return or the Weighted Average Cost of Capital (WACC). It adjusts for both the time value of money and the investment’s risk profile. A higher discount rate reduces the present value, indicating greater risk or higher capital costs. Step 3: Calculate the Present Value of Each Cash Flow Each future cash flow must be discounted to its present value using the formula:

The Present Value of Each Cash Flow, Formula:

The Present Value of Each Cash Flow, Formula:

PV = CFₜ / (1 + r)ᵗ

Where:

- PV = Present Value

- CFₜ = Cash Flow in year t

- r = Discount Rate

- t = Year number

- Step 4: Calculate the Terminal Value Since companies operate beyond the forecast period, the terminal value (TV) accounts for the residual value after the final forecast year. It can be calculated using the Perpetuity Growth Model:

Formula (Perpetuity Growth Model):

Formula (Perpetuity Growth Model):

TV = CFₙ₊₁ / (r - g)

Where:

- CFₙ₊₁ = Cash Flow of the year following the projection period

- g = Perpetual Growth Rate

- Step 5: Discount the Terminal Value to Present Value Once the terminal value is calculated, discount it to its present value using the same rate applied to cash flows.

- Step 6: Add the Present Values Together The final DCF value is obtained by summing the present values of all forecasted cash flows and the discounted terminal value:

Formula:

Formula:

DCF Value = Σ [ CFₜ / (1 + r)ᵗ ] + [ TV / (1 + r)ⁿ ]

Illustrative Example

Illustrative Example

A company projects free cash flows of SAR 1 million annually for five years, with a discount rate of 10% and a perpetual growth rate of 3%.

After discounting each year’s cash flow and calculating the terminal value, the total DCF valuation equals approximately SAR 11.4 million — representing the current worth of the company’s future cash generation potential.

Why DCF Matters in Business Valuation?

In corporate finance, valuation is both an art and a science. Among various valuation models, the Discounted Cash Flow (DCF) method stands out for one main reason — it captures the intrinsic value of a business based on its ability to generate future cash flows, rather than relying solely on market conditions or accounting figures.

- Reflects True Economic Value DCF focuses on cash, not accounting profits. While accounting metrics such as net income or earnings per share can be influenced by non-cash items like depreciation or provisions, DCF eliminates such distortions by analyzing actual cash inflows and outflows. This makes it a more accurate tool for assessing a company’s true economic potential. Example: Two companies may report identical accounting profits, yet the one generating stronger and more sustainable cash flows will command a higher valuation under the DCF approach.

- Accounts for the Time Value of Money Money today is more valuable than the same amount in the future. DCF integrates this principle by discounting future cash flows to their present value. This adjustment ensures that each projected cash flow is evaluated in today’s terms, leading to more reliable investment or acquisition decisions.

- Enables Strategic Decision-Making DCF models are more than valuing companies; they are also used to assess investment projects, mergers, acquisitions, or capital budgeting decisions. DCF helps finance professionals determine whether a project creates or destroys value by showing how future returns compare to the initial investment.

- Supports Scenario and Sensitivity Analysis DCF provides the flexibility for financial analysts to test various assumptions — such as revenue growth, operating margins, or discount rates — and understand their impact on valuation. This makes it an essential tool for risk assessment, particularly in uncertain or volatile markets.

- Enhances Investor Confidence Investors and stakeholders value transparency and logic in valuation. A well-structured DCF model, supported by clear assumptions and sound financial data, communicates credibility and analytical rigor, two qualities critical to investor trust and decision-making.

Limitations and Challenges of the Discounted Cash Flow (DCF) Method

While the Discounted Cash Flow (DCF) method is one of the most respected valuation models in finance, it is not without limitations. Its reliability depends heavily on the quality and accuracy of the assumptions made — particularly regarding future cash flows, discount rates, and terminal value.

Understanding these limitations is essential for interpreting DCF results correctly and applying them responsibly in financial decision-making.

- Dependence on Assumptions and Forecasts The DCF model is only as accurate as the forecasts that drive it. Estimating future revenues, expenses, and growth rates involves uncertainty, especially in volatile markets or emerging industries. Even small errors in projections can lead to significant variations in valuation results. Example: A minor change of 1% in the discount rate or long-term growth assumption can cause a million-dollar difference in the estimated company value.

- Sensitivity to the Discount Rate Selecting the appropriate discount rate is one of the most challenging aspects of DCF analysis. The rate should reflect the risk profile of the business and market conditions, but determining the exact rate often involves judgment. A higher discount rate lowers the present value, while a lower rate inflates it, meaning small adjustments can disproportionately impact valuation.

- Difficulty in Estimating Terminal Value The terminal value (TV), representing the value of the business beyond the forecast period, often accounts for more than half of the total DCF valuation, which means that any incorrect assumption about long-term growth or discount rates can significantly distort the results. Relying too heavily on the terminal value also reduces the DCF sensitivity to near-term operational performance.

- Complexity and Data Intensity DCF requires detailed financial modeling, comprehensive data, and in-depth market understanding. For small businesses or startups with limited financial history, obtaining reliable inputs for future cash flow projections is challenging, often leading to speculative results.

- Less Useful in Highly Uncertain or Cyclical Industries Projecting stable cash flows becomes difficult for companies in industries that experience rapid technological shifts, market disruptions, or cyclical demand (such as energy, real estate, or technology). In such cases, DCF may fail to reflect the real market value, and alternative methods like comparables Or precedent transactions may also be more practical.

- Time-Consuming and Prone to Bias Because DCF involves multiple assumptions and manual calculations, it can be time-consuming and subject to analyst bias. If assumptions are overly optimistic or conservative, the final valuation may reflect the analyst’s expectations rather than objective financial reality.

Comparing DCF with Other Valuation Methods

Valuing a company is not a one-size-fits-all process. Each valuation method offers unique insights depending on the purpose, data availability, and business context. While the Discounted Cash Flow (DCF) approach emphasizes intrinsic value based on future performance, other methods rely on market evidence or asset values.

Understanding how DCF compares with these models helps financial professionals choose the most appropriate approach for their analysis.

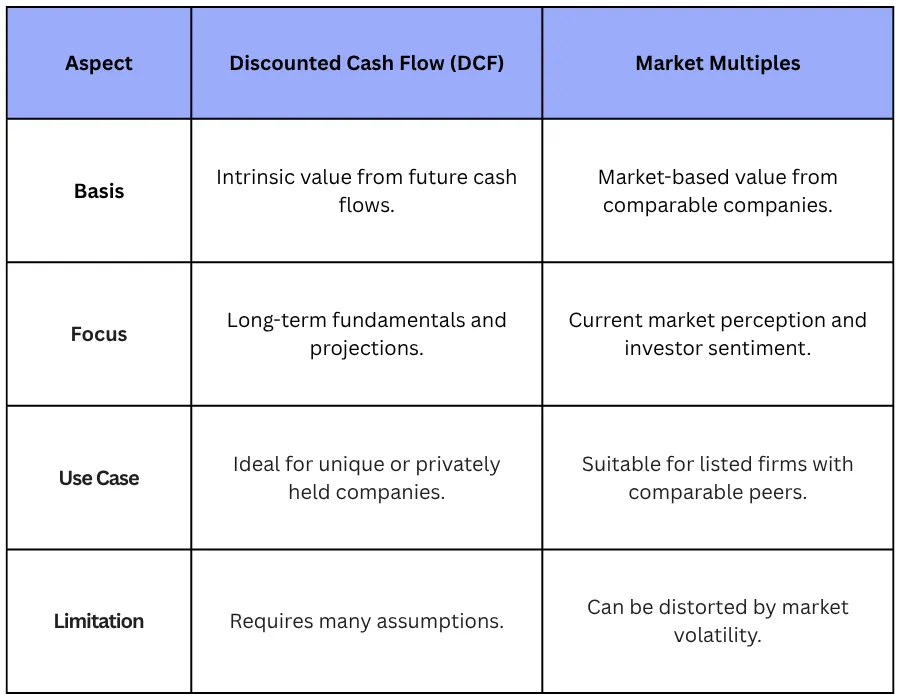

1. DCF vs. Market Multiples Method

The Market Multiples Method (or Relative Valuation) estimates a company’s value based on how similar companies are priced in the market — using ratios like P/E (Price-to-Earnings), EV/EBITDA, or P/B (Price-to-Book Value). DCF is more analytical and future-oriented, while the multiples approach is faster and reflects market trends. Professional analysts often use both DCF for intrinsic valuation and multiples as a market reality check.

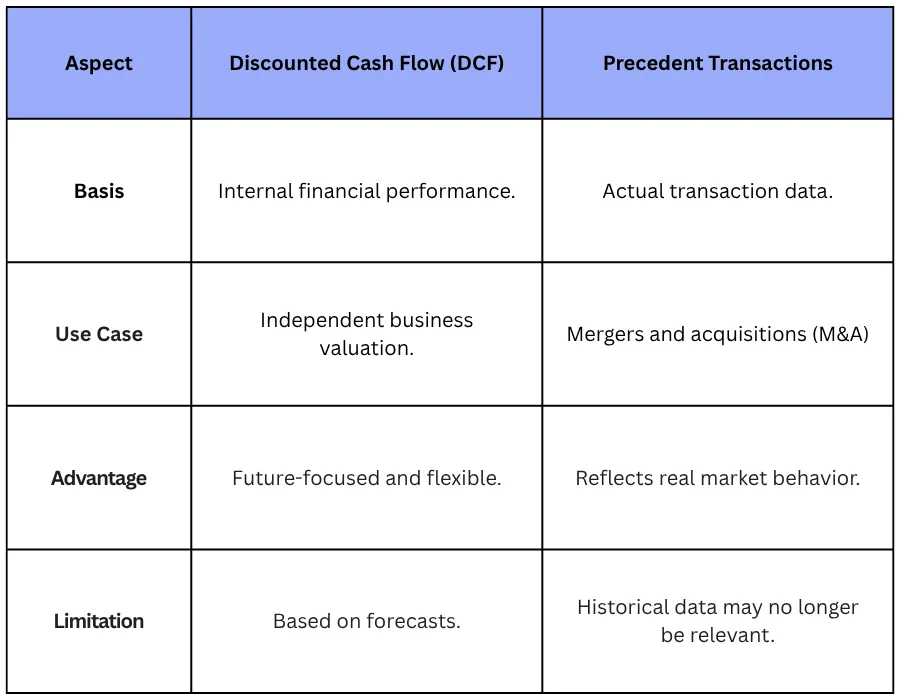

2. DCF vs. Precedent Transactions Method

The Precedent Transactions Method values a business by analyzing past acquisition prices of similar companies. It reflects the actual market prices that buyers had paid, incorporating control premiums or strategic synergies. While DCF shows the company’s intrinsic worth, precedent transactions demonstrate what buyers were willing to pay. Combining both provides a balance between theory and real-world pricing.

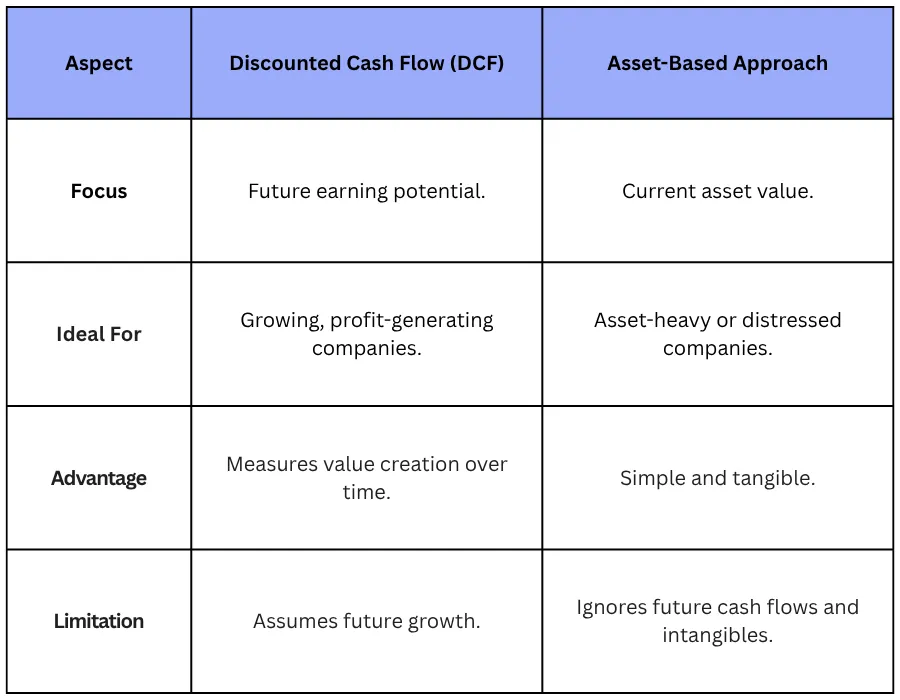

3. DCF vs. Asset-Based Valuation

The Asset-Based Valuation method determines a company’s worth based on the value of its assets minus liabilities — essentially its net book value. It is often used for capital-intensive or liquidation-based scenarios. DCF captures the business's going-concern value, while the asset-based approach provides a floor value, useful in liquidation or restructuring cases.

Complementary Use of Valuation Methods

Complementary Use of Valuation Methods

Experienced financial professionals rarely rely on one model alone. Instead, they triangulate value using DCF, market multiples, and transaction analysis to ensure precision and market alignment, which supports better communication with investors and stakeholders.

Each valuation model serves a different purpose:

- DCF reveals intrinsic value based on future cash flows.

- Multiples mirror market sentiment.

- Precedent transactions represent actual deal behavior.

- Asset-based methods reflect tangible worth.

know more about: Understanding Internal Rate of Return (IRR) in Finance

How Wafeq Helps with Financial Modeling and Valuation

Building a reliable Discounted Cash Flow (DCF) model requires more than technical knowledge — it demands access to accurate financial data, efficient reporting tools, and real-time insights. This is where Wafeq empowers finance teams and business leaders by simplifying data management and improving decision-making accuracy.

- Streamlined Financial Data Collection A strong DCF model depends on reliable input data such as cash inflows, expenses, and growth projections. Wafeq centralizes all financial operations — from invoicing and expense tracking to payments and reconciliations — ensuring that every cash movement is accurately recorded and instantly accessible. This eliminates manual data entry and reduces the risk of errors that often distort valuation results.

- Automated Cash Flow Visibility DCF analysis starts with forecasting future cash flows, and Wafeq simplifies this through automated cash flow reports that present real-time inflows and outflows. Finance teams can easily identify trends, evaluate liquidity, and project future performance, forming a reliable foundation for DCF-based valuations.

- Integration with Accounting and ERP Systems Wafeq integrates seamlessly with major accounting and ERP systems for finance professionals who manage complex operations. This allows continuous synchronization between recorded transactions and analytical models, ensuring consistency between operational data and valuation assumptions.

- Advanced Reporting and Analytics With customizable dashboards and dynamic reporting, Wafeq enables users to generate profit and loss, balance sheet, and cash flow statements — all essential components of a DCF model. The platform’s analytical tools help CFOs and financial controllers evaluate performance metrics, monitor working capital, and refine valuation inputs with precision.

- Time and Cost Efficiency Manual financial modeling can be time-intensive and error-prone. By automating repetitive accounting and reporting tasks, Wafeq allows finance professionals to dedicate more time to strategic analysis — such as evaluating project feasibility, investment returns, or corporate valuation using DCF and other methods.

- Enhanced Accuracy and Decision Support Through centralized financial management and real-time insights, Wafeq helps ensure the data driving valuation models is complete, accurate, and up-to-date. This enhances the credibility of financial reports and strengthens the confidence of stakeholders in valuation results and investment decisions.

Read Also: Cash Flow Management Strategies: How to Achieve Financial Stability for Your Business

The Discounted Cash Flow (DCF) method remains one of the most powerful and widely used techniques for valuing businesses, investments, and projects. Its strength lies in its ability to capture the time value of money, ensuring that future cash flows are adjusted for their present worth. However, its accuracy depends on the reliability of assumptions — particularly growth rates, discount rates, and cash flow projections.

So, finance professionals, investors, and business owners must use DCF as a strategic tool, supported by accurate data and scenario analysis, to make sound decisions.

FAQs about Discounted cash flows

What is the main purpose of the DCF method?

The DCF method aims to determine a business or investment's actual value by estimating future cash flows and discounting them using a rate that reflects risk and cost of capital.

What are the main inputs required for DCF analysis?

Key inputs include projected cash flows, discount rate, growth rate, and terminal value. These assumptions determine the accuracy of the valuation outcome.

What are the main advantages of using DCF?

It provides a detailed, forward-looking view of value, incorporates the time value of money, and allows scenario analysis under different assumptions.

What are the limitations of DCF?

DCF is highly sensitive to assumptions — small changes in growth or discount rates can significantly alter valuation results. It also requires consistent, reliable data.

By combining financial expertise with smart automation tools like Wafeq, businesses across the region can ensure that every valuation reflects real performance, reliable data, and long-term growth potential.

By combining financial expertise with smart automation tools like Wafeq, businesses across the region can ensure that every valuation reflects real performance, reliable data, and long-term growth potential.

.png?alt=media)